Resources

What We Learned Mapping 2,800 Web3 Companies

Testing strong narratives in earlier Web3 cycles.

Written By

Bradley Stone

Date

Category

Insights

Length

There were strong narratives in earlier Web3 cycles: DAOs would replace companies, self-custody would make banks obsolete, and tokenization would start with art and end with everything.

To test what actually happened, we mapped 2,800+ Web3 projects and organizations, alongside 5,860+ products, 2,330+ legal entities, and 1,530+ assets. The picture that emerges is less “replacement” and more integration: Web3 matured by fitting into existing institutional and regulatory rails.

The evidence shows up across categories. In governance, traditional companies outnumber DAOs 29:1. In custody and wallets, embedded wallets (the kind users barely notice) are growing faster than hardware wallets. In tokenization, real-world assets (RWAs) have quietly overtaken NFTs by category count. In data infrastructure, compliance tooling is approaching the scale of analytics platforms—tracking with a more regulated, operationally mature ecosystem.

Whatever the ideological starting point, the center of gravity shifted. Web3 now often comes with a legal entity, a compliance function, and a banking partner. What remains is an industry that looks less like an exit from traditional finance and more like an attempt to upgrade parts of it.

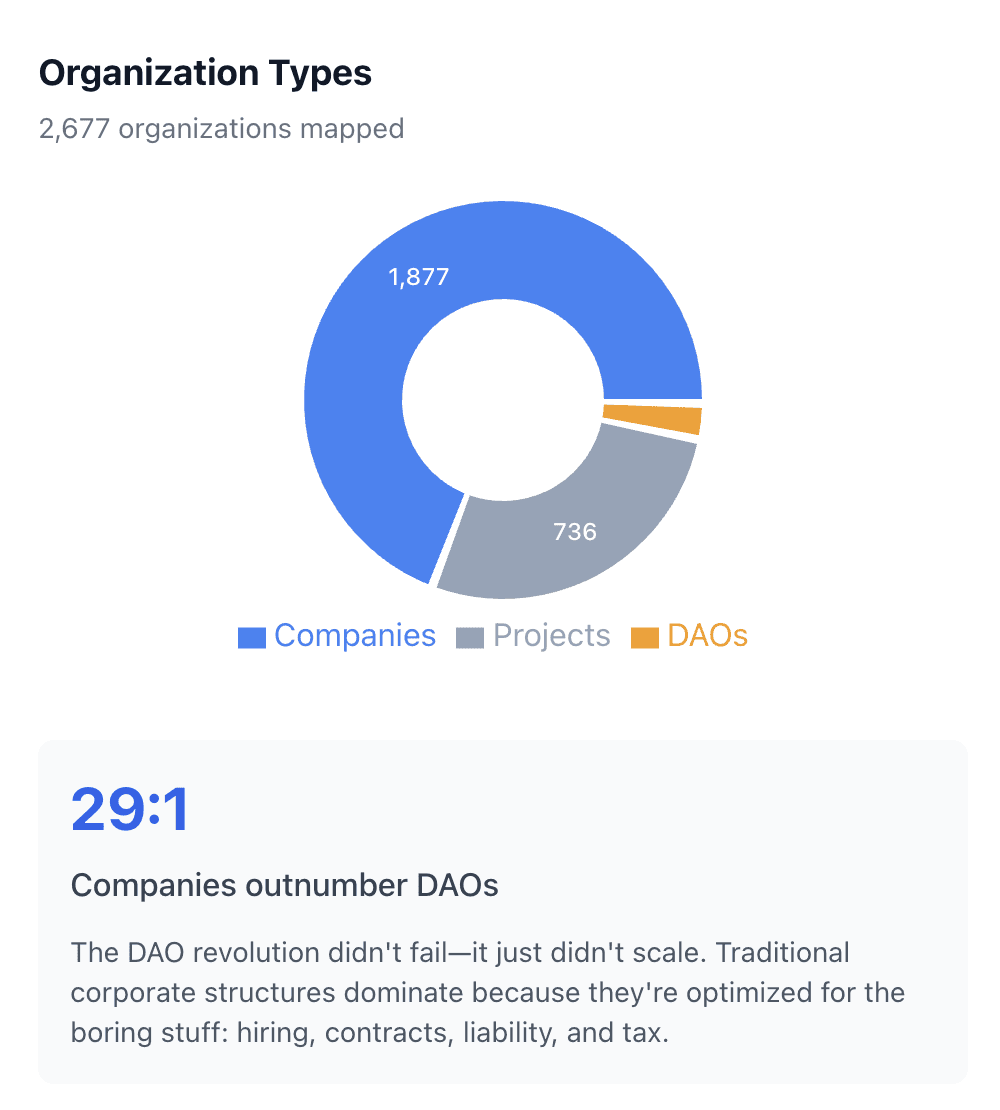

Corporate Takeover

The most striking ratio in our dataset is how sharply companies outnumber DAOs, and with many organizations not able to make the full DAO commitment. Of the 2,600+ organizations we could classify:

1,877 are companies — registered entities with directors, shareholders, and traditional governance

736 are "projects" — hybrid structures, often a foundation paired with a development company

64 are DAOs — genuine decentralized governance with on-chain voting

Traditional companies outnumber DAOs 29 to 1.

We suppose that's because as global regulations matured, focusing on a DAO structure was no longer the most practical approach for many projects. DAOs struggle with the mundane, like signing leases, hiring employees, managing payroll, limiting liability, filing taxes. When Uniswap needs to negotiate a partnership or Aave needs to respond to a regulator, someone has to sign. That someone needs a legal entity behind them.

The "project" category (around 736 organizations) tells the real story of how the industry adapted. These are the compromises: a Cayman foundation holding the token, a Swiss AG employing the developers, a Delaware LLC handling US operations. Decentralization as legal architecture rather than organizational reality.

The DAO dream isn't dead. But it's niche. The 64 genuine DAOs in our dataset tend to be protocol treasuries and grant committees—functions where slow, distributed decision-making is acceptable. For everything else, there's a company.

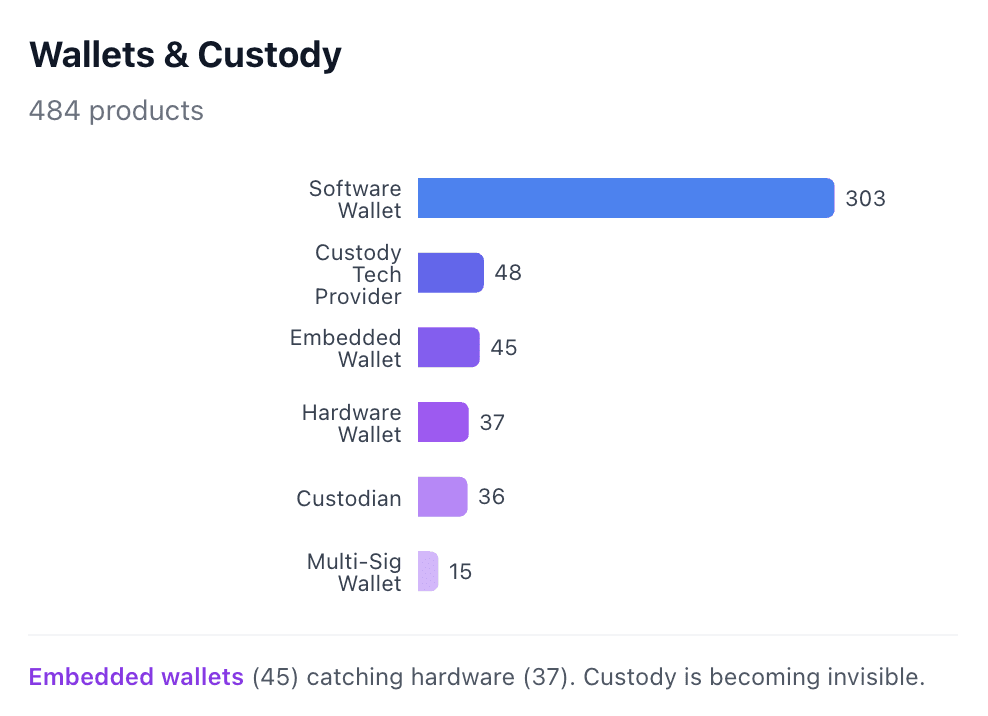

The Disappearing Wallet

The early crypto mantra was "not your keys, not your crypto." Self-custody the entire point. Our data suggests users have more options for custody than ever before, and most of them keep users in control.

484 custody-related products break down like this:

Category | Count | Share |

|---|---|---|

Software Wallet | 303 | 63% |

Custody Technology Provider | 48 | 10% |

Embedded Wallet | 45 | 9% |

Hardware Wallet | 37 | 8% |

Custodian | 36 | 7% |

Multi-Sig Wallet | 15 | 3% |

Software wallets dominate in terms of the number of products. The sheer amount of options don't necessarily reflect quality, but fortunately, we primarily track that by screening for active and genuine projects in our dataset.

The deeper read is that embedded wallets (45) have nearly caught hardware wallets (37). Embedded wallets are the ones users never see. They're the wallet abstracted behind a login, the keys generated and stored so the user can simply use the app. No seed phrases, browser extensions, or friction. Convenience beats ideology, not because users don't care about security, but because they care about being able to use the product more. It's neat to see trends like this while scouring our dataset.

Meanwhile, custody technology providers (48) now outnumber actual custodians (36). The infrastructure layer is growing faster than the service layer. If you're judging it by the number of profiles in our dataset, the trend is institutions want custody solutions built into their existing systems, not another vendor relationship.

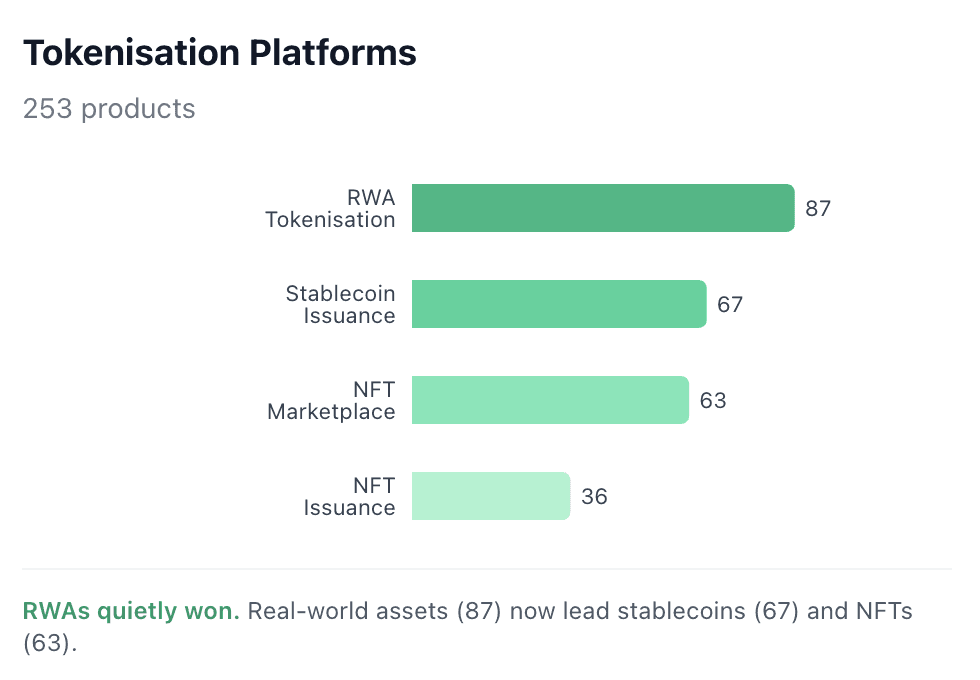

From JPEGs to Treasury Bonds

When tokenization meant 'PFP', most people didn't know what 'tokenization' even meant. The market has evolved, and perhaps gotten more serious.

~253 tokenization products tell a story of shifting priorities:

Category | Count | Share |

|---|---|---|

RWA Tokenization Platform | 87 | 34% |

Stablecoin Issuance | 67 | 26% |

NFT Marketplace | 63 | 25% |

NFT Issuance Platform | 36 | 14% |

Real-world asset tokenization (87 products) has become the largest category, which is bigger than stablecoins, or NFT marketplaces. Obviously, stablecoins are what keep the fire burning around here, and we aren't comparing onchain data at The Grid. However, the breakdown of valid, active profiles in our dataset still suggest a growing trend: The infrastructure built for speculation is increasingly supporting familiar TradFi instruments like treasury bonds, real estate, and private credit.

This is the quiet pivot that happened while the NFT discourse dominated CryptoTwitter. In 2021, tokenization meant Bored Apes. In 2026, it means BlackRock money market funds on Ethereum. The technical stack is similar, but the customer base is entirely different.

We track ~63 NFT marketplaces, meaning clearly that sector hasn't disappeared, but they've been eclipsed in growth and importance. Consumer speculation was the use case that proved the technology. Institutional adoption is the use case that's scaling it. RWA platforms don't generate viral moments, but they generate revenue. And they're what institutional allocators actually want to buy.

At the core of tokenization and RWAs, stablecoins (~67 products) remain the on-ramp for both retail and institutions, and we've seen a big increase in stablecoin issuance companies making it into our dataset.

We suppose this all means you can expect more brokers than art galleries in Web3 from here on.

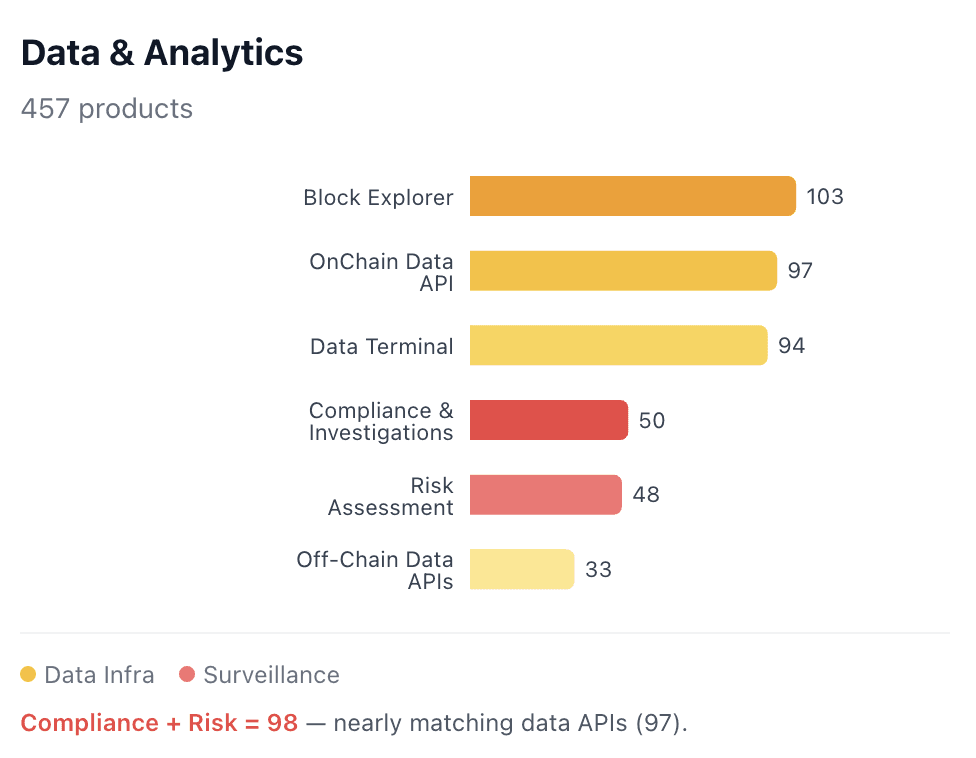

The Surveillance Layer

Blockchains are transparent by design. Every transaction is public, every wallet is auditable. Naturally, we've ended up with loads of analytics products (~457) to utilize that transparency and translate it into something digestible and useful for end users.

Category | Count | Share |

|---|---|---|

Block Explorer | 103 | 23% |

OnChain Data API | 97 | 21% |

Data Terminal | 94 | 21% |

Compliance & Investigations | 50 | 11% |

Risk Assessment | 48 | 11% |

Off-Chain Data APIs | 33 | 7% |

Pricing Data API | 21 | 5% |

The top three categories (block explorers, data APIs, terminals) are neutral infrastructure. They're the picks and shovels: tools for developers, traders, and researchers to query the chain.

But look at what's right behind them. Compliance and investigations (50) plus risk assessment (48) equals 98 products. When counting active profiles in this category, the surveillance layer is nearly as large as the core data infrastructure (97 OnChain Data APIs).

This is what institutional adoption actually looks like. Banks want to know which wallets have touched sanctioned addresses, which tokens have been through mixers, which counterparties fail their risk models, and so on. You cannot onboard a compliance department without answering these questions. And now there are 98 companies competing to provide those answers.

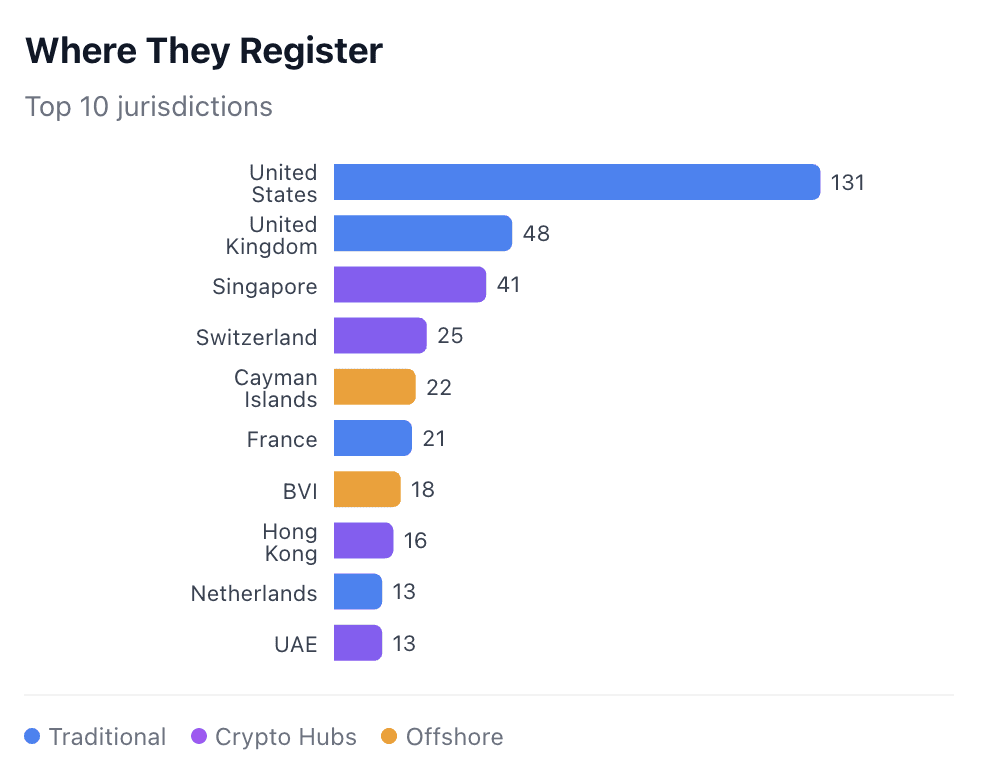

Two Industries, One Name

Web3 technology is borderless. Web3 companies are not.

Top 10 jurisdictions by registered entities:

Jurisdiction | Entities | Type |

|---|---|---|

United States | 131 | Traditional |

United Kingdom | 48 | Traditional |

Singapore | 41 | Crypto Hub |

Switzerland | 25 | Crypto Hub |

Cayman Islands | 22 | Offshore |

France | 21 | Traditional |

British Virgin Islands | 18 | Offshore |

Hong Kong | 16 | Crypto Hub |

Netherlands | 13 | Traditional |

UAE | 13 | Crypto Hub |

The US dominates with 131 entities. That's more than the next two jurisdictions combined. But the composition reveals two distinct industries operating under the same label.

Offshore jurisdictions cluster around tokens. Cayman Islands, BVI, Seychelles, Panama—these are where token-issuing projects incorporate. The structures offer regulatory flexibility, tax efficiency, and liability separation. When a project needs a foundation to hold its treasury and a company to employ its developers, the foundation goes offshore.

Traditional jurisdictions cluster around infrastructure. The US, UK, and EU host the B2B tooling companies—the data providers, custody technology, compliance platforms, and developer tools. These companies look like traditional tech startups because they are. They have venture backing, enterprise sales teams, and are not inextricably tied to any token (though increasingly often manage tokenized assets). They stay onshore because their customers require it.

What This Means

The original vision of Web3 got absorbed into something more familiar.

Governance: DAOs exist, but companies run the industry. The legal wrapper won.

Custody: Self-custody remains possible, but invisible wallets are gaining ground.

Tokenization: NFTs proved the concept. RWAs are scaling it. The speculators tested the early infrastructure that institutions will use to build more buttoned-up platforms.

Data: Transparency became a feature for compliance, not just for users. While you're possibly hearing about the revival of "privacy coins" on social media, the surveillance layer is now built-in.

Geography: Tokens go offshore, infrastructure stays onshore.

The Web3 industry in 2026 doesn't look like the replacement for TradFi that its founders imagined. It looks like an ambitious upgrade, absorbing the technology but not placing too much importance on the ideology. The revolution got compliance departments, legal entities, and banking partners. What remains is less radical and more durable.

For builders, the implication is that the winning products are the ones that make Web3 invisible. Embedded wallets, RWA rails, compliance APIs, tools that institutions can adopt without explaining blockchain to their boards.

For investors, the implication is that the infrastructure layer is where the defensible businesses are being built. Picks and shovels, not tokens.

For the industry, the implication is that absorption was probably always the most likely outcome. The question now is what comes next, and whether anything remains that TradFi can't simply copy.

Why We’re Building This (and What Comes Next)

Manually tracking this space is already impossible. New products launch daily. Companies move their headquarters. Projects rebrand, pivot, and introduce new products and assets. Almost any marketmap or report is out of date the moment it is published.

For us at The Grid, this is precisely the reason to keep going. Because even the thousands of profiles we mapped are a snapshot that is already aging as you read this.

We want to:

Map the serious side of Web3: the entities, products, and relationships that actually touch money, legal requirements, and infrastructure.

Make our own assumptions and biases explicit, so people can interpret the data correctly.

Gradually expand coverage to more ecosystems, more long-tail activity, and more of the cultural and experimental edge, without losing quality.

Improve updates with the goal to get as close to real-time as possible.

Our team has always liked hard problems. Getting to high-quality information in this space is one of them. But if this industry is going to mature, it needs less narrative and more grounded, living maps of what is actually being built and by whom.

What we see in Web3 is not a pure revolution and not a failure either. It’s an adolescent entering adulthood. It's a noisy, very human industry trying to rebuild parts of the financial stack and the internet on new rails, while still living inside the old world’s laws, banks, and funding models.

Our job at The Grid is to increase visibility, so that through the fog we can gather a better picture of how it's all connected, what all of it is for, where it's happening, and where it's going.

Want to explore the data yourself?

If you're building in Web3 or leading an ecosystem, you can see how your project fits into the map.

Explore The Grid: https://explorer.thegrid.id/

Claim Your Profile: https://network.thegrid.id/